{kind=link}

Non-owner automotive insurance coverage gives protection in case you recurrently drive one other individual’s car. Discover out if this kind of auto coverage is for you

At first look, non-owner automotive insurance coverage looks as if a reasonably easy type of protection. It protects you financially in case you get into an accident whereas driving one other individual’s car. However identical to different varieties of auto insurance coverage, there are a number of layers to the type of safety this coverage gives.

On this article, Insurance coverage Enterprise explains how non-owner automotive insurance coverage works. We’ll focus on what this coverage covers and what it doesn’t, and the way a lot protection prices.

For those who’re questioning whether or not this kind of automotive insurance coverage is a worthwhile funding, this information can assist.

Since auto insurance coverage is necessary in virtually all states for everybody working a car, not having your personal automotive doesn’t exempt you. That is the place non-owner automotive insurance coverage turns out to be useful.

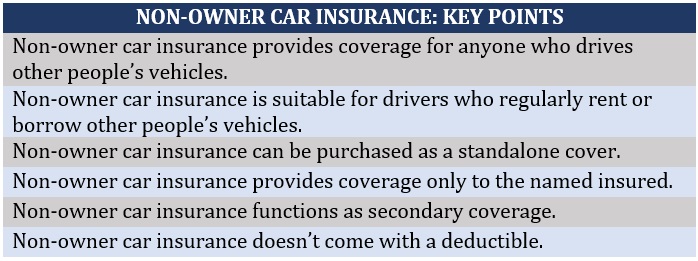

This kind of coverage gives safety for anybody who regularly drives one other individual’s car or these whose private circumstances require them to supply proof of protection. For those who recurrently lease or borrow a relative’s or good friend’s car for private driving, then a non-owner coverage could be a appropriate type of safety.

Many automobile insurers supply non-owner automotive insurance coverage as a standalone coverage, though some supply protection just for present policyholders.

Non-owner car insurance coverage serves as a secondary sort of safety. Which means that in case you get into an accident, the proprietor’s automotive insurance coverage gives protection first as much as the coverage’s limits. As soon as the loss or injury exceeds these limits, your non-owner coverage then picks up the tab.

Non-owner automotive insurance coverage additionally capabilities as a named insured coverage, which means it solely covers the policyholder.

There are some auto insurers that may allow you to add your partner to your coverage, however this isn’t commonplace apply. Usually, in case you and your partner each want non-owner insurance coverage, you will want to take out separate protection.

One other key characteristic of non-owner insurance policies is that you just don’t have to pay a deductible for protection to kick in.

Right here’s a abstract of the important thing factors it’s essential to keep in mind when taking out non-owner automotive insurance coverage.

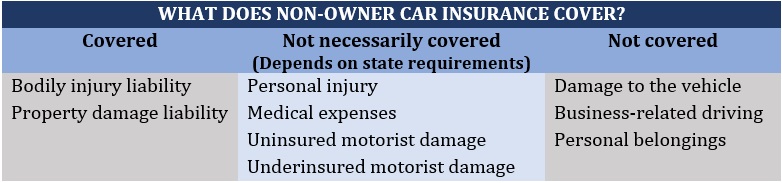

Non-owner automotive insurance coverage insurance policies are designed primarily to supply legal responsibility safety. Legal responsibility automotive insurance coverage protects you financially if in case you have been discovered legally accountable for an accident that ends in one other individual’s harm, dying, or property injury.

This kind of protection is required in virtually all states, that’s why it’s usually thought of the muse of any automotive insurance coverage coverage.

Legal responsibility automotive insurance coverage gives two varieties of protection:

- Bodily harm legal responsibility: This pays for the medical prices of the individual you injured in an accident and your authorized bills in case you get sued. Some insurance policies additionally cowl a 3rd social gathering’s misplaced earnings and funeral bills.

- Property injury legal responsibility: This compensates one other individual for property injury and losses ensuing from an accident you brought on. It additionally covers authorized bills arising from a lawsuit, in addition to settlement prices.

Get a deeper understanding of how legal responsibility automotive insurance coverage works on this complete information.

Non-owner automotive insurance coverage sometimes contains your state’s minimal protection necessities, though you should purchase a coverage with larger limits to offer you prolonged safety. And since it’s designed to fulfill state-mandated coverages, your coverage can even supply:

- Private harm safety (PIP): This covers you and your passenger’s medical and therapy bills in case you get injured in an accident. It additionally pays for misplaced wages and the price of family companies in case your harm prevents you from performing such duties. PIP protection is required in no-fault states.

- Medical funds (MedPay) protection: This pays for you and your passenger’s medical and therapy prices, no matter who brought on an accident. MedPay, nevertheless, doesn’t cowl misplaced earnings. This kind of protection is necessary in Maine and Pennsylvania.

- Uninsured/underinsured motorist (UM/UIM) protection: UM insurance policies compensate you and your passengers for accidents and broken property in case you’re hit by an uninsured driver. This may occasionally additionally cowl hit-and-run accidents. UIM protection, in the meantime, kicks in if the at-fault driver’s insurance coverage shouldn’t be sufficient to cowl all the value of an accident. UM and UIM insurance policies are sometimes bundled collectively.

We’ve compiled a listing of all of the minimal protection necessities for every state in a single neat desk in our full information on how automotive insurance coverage works.

Non-owner automotive insurance coverage doesn’t have among the options current in commonplace auto insurance policies. Right here’s a listing of some incidents not lined by your non-owner insurance coverage and what insurance policies can present protection as a substitute.

- Damages to the car: Non-owner insurance policies don’t cowl injury or losses to the car you’re driving. These are sometimes lined by the proprietor’s collision and complete automotive insurance coverage insurance policies.

- Enterprise-related driving: For those who’re driving a company-owned car, it must be lined by your employer’s industrial auto insurance coverage coverage. If the enterprise is renting or borrowing the car you’re utilizing for industrial functions, then your organization must take out employed and non-owned automotive insurance coverage. Each situations will not be lined by non-owner automotive insurance coverage.

- Belongings stolen from the car: Private possessions left contained in the autos aren’t included in your non-owner protection. So, it gained’t pay out if these are broken or stolen. Such incidents, nevertheless, could also be lined by your householders’ or renters’ insurance coverage coverage.

Right here’s a abstract of what non-owner automotive insurance coverage covers and what it doesn’t.

The common value of a non-owner automotive insurance coverage coverage is round $795 per yr primarily based on the assorted value comparability and insurer web sites that Insurance coverage Enterprise checked out. The quantity is for a coverage with 100/300/100 legal responsibility protection.

The premiums you pay, nevertheless, could also be significantly decrease or larger relying on a variety of things. These embrace:

- Your age: The youthful and fewer driving expertise you may have, the upper the premiums it’s essential to pay.

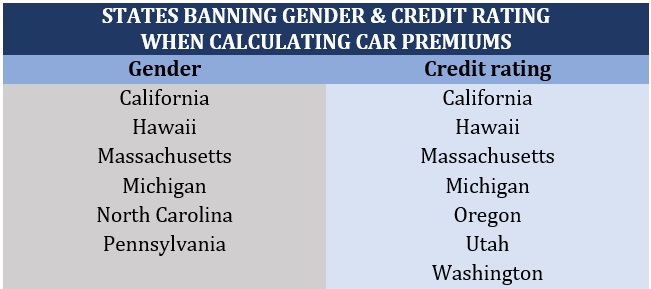

- Your gender: Males sometimes pay extra for protection as they’re statistically extra susceptible to accidents than ladies. The disparity is extra pronounced amongst youthful drivers however sometimes ranges off as drivers age.

- The place you reside: Every state imposes totally different necessities relating to automotive insurance coverage, which may impression the value you pay for protection.

- Your driving historical past: Accidents and main violations can elevate the price of non-owner insurance policies. Conversely, having a spotless driving file qualifies you for reductions.

- Your credit standing: Insurers usually view drivers with poor credit score scores as extra more likely to file claims sooner or later. This raises their premiums.

- The extent of protection: The minimal necessities states impose are sometimes not sufficient to cowl all the value of an accident. That’s why it’s advisable to buy insurance policies past these state minimums. You’ll pay extra in premiums, however you’ll additionally get the next stage of safety.

Some states, nevertheless, prohibit auto insurance coverage firms from utilizing gender and credit standing in calculating premiums. These states are listed within the desk under.

Automobile insurance coverage is likely one of the greatest prices related to proudly owning and working a car, however there are methods to slash premiums. Get sensible suggestions and methods on how one can entry low-cost automotive insurance coverage.

Non-owner automotive insurance coverage is designed for drivers who regularly use different folks’s autos. However you want it greater than others if:

You recurrently borrow different folks’s autos

Whereas the proprietor’s automotive insurance coverage gives legal responsibility protection in case of an accident, you’ll be on the hook for the remaining bills if these exceed the coverage’s limits. Non-owner insurance coverage helps cowl the associated fee as much as the coverage’s limits.

You usually lease autos from automotive leases

For those who’re renting a car from automotive rental firms, you can even buy rental automotive insurance coverage in-house. Nevertheless, this usually prices greater than a normal non-owner automotive insurance coverage coverage. If you wish to save on premiums, getting non-owner auto protection is the way in which to go.

You regularly depend on car-sharing companies

Automobile-sharing companies supply in-house protection, however that is usually the naked minimal. If you’d like the next stage of safety, it’s finest to get non-owner insurance coverage.

You don’t need a hole in your automotive protection

Having a spot in automotive protection ends in larger premiums when you resolve to buy insurance coverage once more, even in case you didn’t personal a car throughout that interval. To keep away from this, it pays to take out non-owner automotive insurance coverage.

You’re required to supply an SR-22 certificates

For those who’re within the technique of getting your license reinstated after a significant site visitors violation or legal conviction, chances are you’ll want to supply proof of protection within the type of an SR-22 certificates. Relying on the state, chances are you’ll want to take action even in case you don’t personal a automotive. That is the place non-owner automotive insurance coverage turns out to be useful. Your insurer information the SR-22 (or FR-44 in Florida and Virginia) doc in your behalf to show that you’ve got a minimum of minimal protection.

Non-owner automotive insurance coverage, nevertheless, doesn’t go well with everybody. You may skip this type of protection if:

Somebody out of your family owns the automotive you recurrently borrow

You don’t want non-owner insurance coverage if the automotive you usually borrow belongs to somebody you reside with. It’s because you could be named as an extra insured of their coverage.

You usually borrow the identical car from somebody exterior your house

Insurers sometimes require policyholders to call each driver who regularly makes use of their car of their coverage. This implies you could be lined below the proprietor’s automotive insurance coverage.

You hardly ever drive

Non-owner car insurance coverage shouldn’t be for you in case you hardly ever drive. It could be higher – and less expensive – in case you simply buy auto insurance coverage from a rental firm each time you lease or simply depend on the proprietor’s automotive coverage if an accident happens.

You’re driving a car that your organization owns

For those who’re utilizing a company-owned car for business-related duties, you need to be lined below your employer’s industrial auto insurance coverage. Simply just be sure you’re not utilizing the car to run private errands or for recreation.

What does non-owned auto imply in automotive insurance coverage?

In automotive insurance coverage, a non-owned auto is any car that’s recurrently pushed by a non-owner. However since automotive insurance coverage is legally required for anybody working a car, non-owners should additionally take out protection, aptly referred to as non-owner automotive insurance coverage. This coverage is designed to supply safety for many who regularly drive a car that one other individual owns.

Are you able to get automotive insurance coverage in case you don’t personal a automotive?

Even in case you don’t personal a car, you’ll be able to nonetheless entry protection within the type of non-owner automotive insurance coverage. This kind of coverage protects you from the monetary legal responsibility of paying for bodily harm and property injury from an accident you brought on. Non-owner automotive insurance coverage fits you in case you regularly lease or borrow a car to your private actions.

What’s going to occur to your non-owner automotive insurance coverage after you’ve purchased a automotive?

When you’ve purchased your personal car, it’s essential to take out a normal automotive insurance coverage coverage. Some insurers might can help you convert your non-owner insurance coverage to a normal coverage. However since common auto insurance coverage sometimes prices extra, you may additionally have to pay larger premiums.

Automobile insurance coverage could be a sophisticated type of protection, particularly in case you don’t have ample business information and expertise. If you wish to acquire a deeper understanding of the auto insurance coverage area, you’ll be able to go to our Motor & Fleet Information Part. Bookmark this web page to simply entry breaking information and the most recent business developments.

Have you ever skilled taking out non-owner automotive insurance coverage? How was it? We’d like to see your story within the feedback part under.

Sustain with the most recent information and occasions

Be a part of our mailing checklist, it’s free!